Economic Issues

- Gross Domestic Product (GDP) is the total value of output of goods and services in a country in one year.

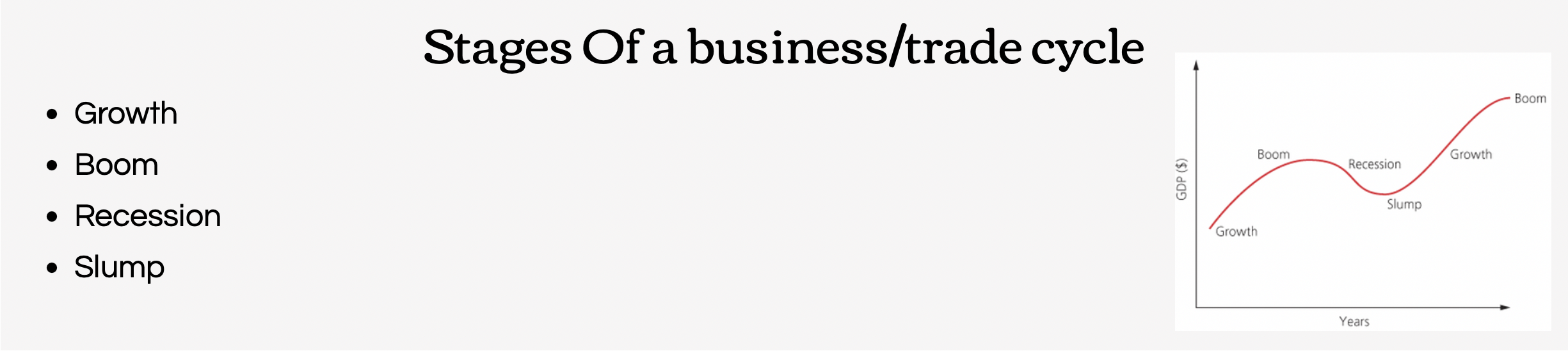

- Recession is when there is a period of falling GDP.

- Inflation is the increase in the average price level of goods and services over time.

- Unemployment exists when people who are willing and able to work cannot find a job.

- Economic growth is when a country’s GDP increases – more goods and services are produced than in the previous year.

- Balance of payments records the difference between a country’s exports and imports.

- Real income is the value of income, and it falls when prices rise faster than money income.

- Exports are goods and services sold from one country to other countries.

- Imports are goods and services bought in by one country from other countries.

- Exchange rate is the price of one currency in terms of another, for example, £1 : $1.5.

- Exchange rate depreciation is the fall in the value of a currency compared with other currencies.

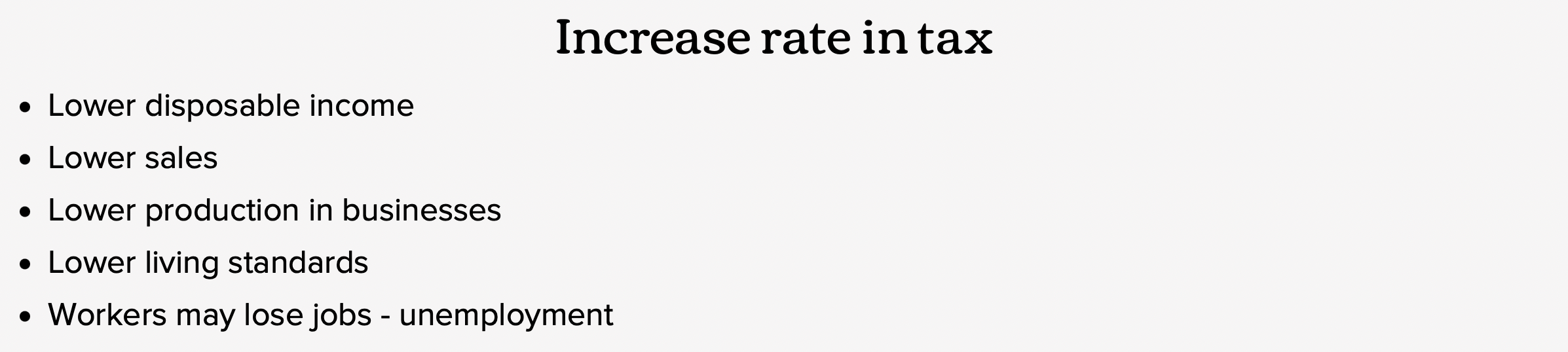

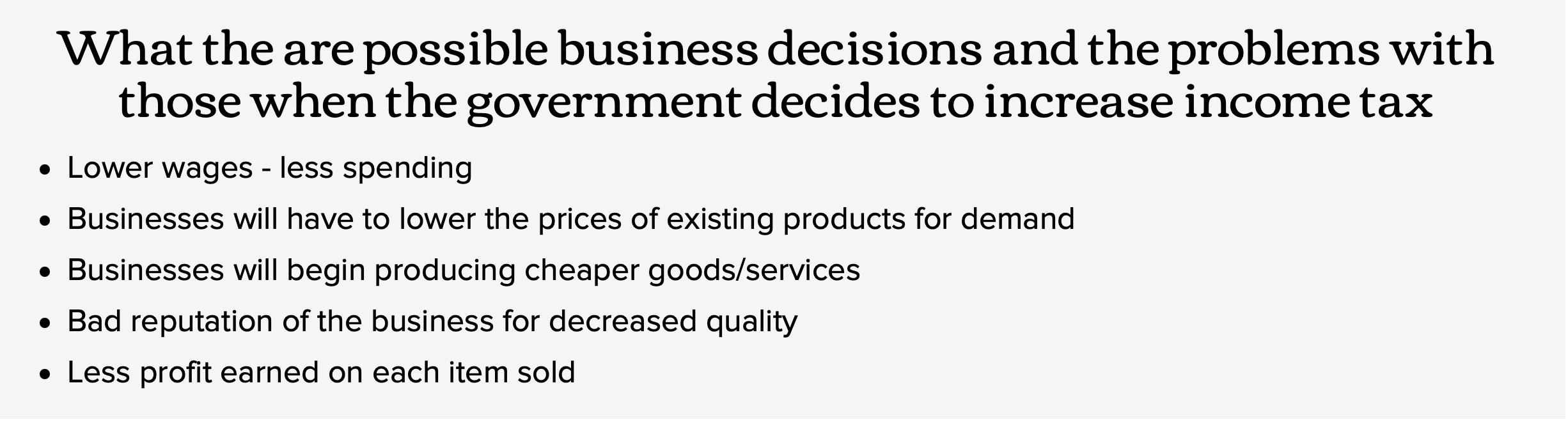

- Fiscal policy is any change by the government in tax rates or public sector spending.

- Direct taxes are paid directly from incomes, for example, income tax or profits tax.

- Indirect taxes are added to the prices of goods and taxpayers pay the tax as they purchase the goods, for example, VAT.

- Disposable income is the level of income a taxpayer has after paying income tax.

- Import tariff is a tax on an imported product.

- Import quota is a physical limit on the quantity of a product that can be imported.

- Monetary policy is a change in interest rates by the government or central bank, for example, the European Central Bank.

- Exchange rate appreciation is the rise in the value of a currency compared with other currencies.

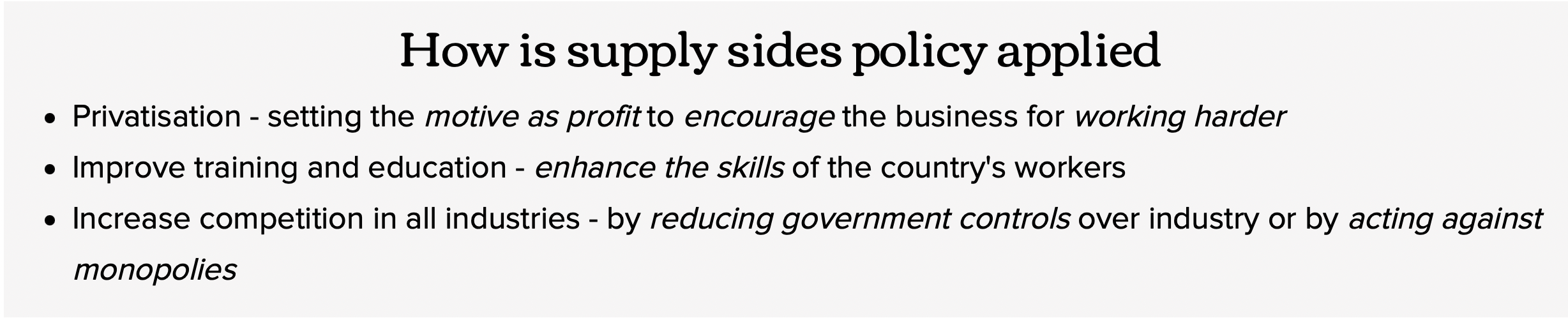

- Supply side policies try to increase the competitiveness of industries in an economy against those from other countries. Policies to make the economy more efficient.

| economic_issues.pdf |